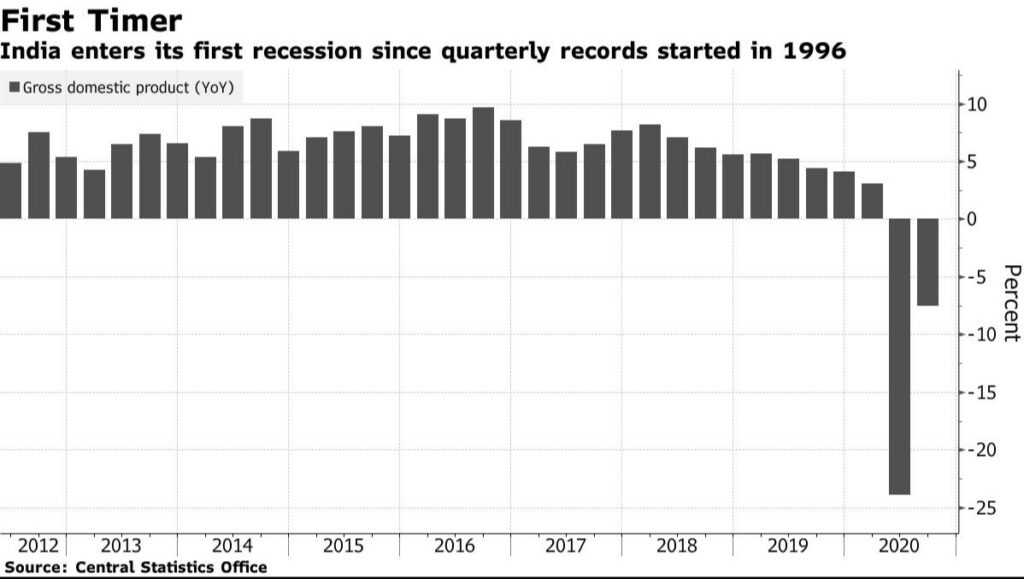

With the lingering effects of COVID-19 induced lockdown still prevailing, India entered into an unprecedented ‘technical recession’ with its economy contracting 7.5 per cent in the July-September quarter (Q2), the National Statistical Office said on Friday.

However, the economy fared well in Q2 as the lockdown restrictions eased in comparison to Q1 when the contraction was a massive 23.9 per cent. The figures are also better than the anticipations of most rating agencies and analysts. While most had estimated a contraction of around 10 per cent, the Reserve Bank of India had projected an 8.6 per cent decline in the second quarter.

What is a technical recession?

A technical recession is a term used to describe two consecutive quarters of decline in output. In the case of a nation’s economy, the term usually refers to back-to-back contractions in real GDP.

The most significant difference between a ‘technical recession’ and a ‘recession’ is that while the former term is mainly used to capture the trend in GDP, the latter expression encompasses an appreciably more broad-based decline in economic activity that covers several economic variables including employment, household and corporate incomes and sales at businesses.

Another key feature of a technical recession is that it is most often caused by a one-off event (in this case, the COVID-19 pandemic and the lockdowns imposed to combat it) and is generally shorter in duration.

Impact of COVID-19 lockdown

The National Statistical Office said that its estimates are hampered to some extent by the restrictions imposed in the first quarter of this year during the national lockdown due to COVID-19.

“Though the restrictions have been gradually lifted, there has been an impact on economic activities. In these circumstances, some other data sources such as GST, interactions with professional bodies, etc. were also referred to for corroborative evidence and these were clearly limited,” it noted.

Key sectors register growth

Agriculture, which was the only sector to record growth in Q1 grew at the same pace of 3.4 per cent in the second quarter. Interestingly, this time around, the manufacturing gross value-added (GVA) staged a sharp recovery to record 0.6 per cent growth after collapsing 39.3 per cent in the last quarter.

Electricity, gas, water supply and other utility services also recorded 4.4 percent growth, recovering from a 7 per cent contraction in Q1.

But it remained a bleak quarter for several sectors, including mining, services such as retail trade and hotels, construction and financial services.

“We should be cautiously optimistic as the economic impact is primarily due to the pandemic and the sustainability of the recovery depends critically on the spread of the pandemic. The government remains ready to come up with calibrated responses,” said Chief Economic Adviser (CEA) Krishnamurthy Subramanian to The Hindu.

He stressed that there could be neither too much exuberance nor excessive pessimism at this point. Citing the uncertainty caused by the pandemic, Subramanian said the ‘V-shaped recovery’ should continue but it is difficult to be sure about positive growth returning in the remaining two quarters of this year. Finance Minister Nirmala Sitharaman had earlier suggested that the economy could record near-zero growth in 2020-21.